| ||||||||||||||

| ||||||||||||||

|

|

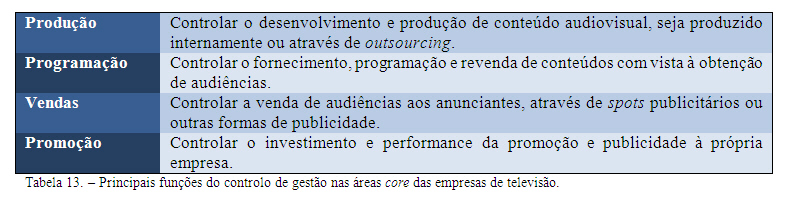

3.4 - Management Control in Television 3.4.1 - Background The importance of management control to an organization was already introduced. The management control plays a fundamental role in evaluating the performance segment, not just as a user of the information, but also in building the model. It is therefore important to introduce the management control in television, their peculiarities, the main difficulties and instruments. According to Geisler (2000), the functions of management control in television varies among countries, types and size of company. The management control systems in public and private TV reflect the different missions of the business. Management control has evolved from its origins to accounting and financial functions that involve budgeting, planning, reporting, assessment and management accounting. To understand the role of management control is essential to distinguish management control of the controller as an individual, since this function is a collaborative effort between the manager and controller. The controller is basically an internal consultant (Geisler, 2000). Such as setting targets or the preparation of action plan, the management control is primarily a function of the area manager. This needs to monitor the results of their decisions, compared with forecasts, to identify the causes of deviations and take corrective action. In this context, the controller appears as a co-pilot of the manager, providing the necessary data so that it can develop its estimates or conducting analysis for decision support (Jordan et al., 2007). Management control can be applied across the enterprise, to all areas. You may be centralized or functionally divided between different areas of the company. According to Geisler (2000), the management control can not thus be examined from a global perspective to the company, but considered individually taking into account the different areas in which it operates. The core processes in the business of television, can be divided into production, programming, sales and promotion. Despite acting in other areas such as human resource management or strategic management, since these are the core business processes, the better distinguish between the management control in television and have their peculiarities, are the topics covered. The form of management control action in each area varies depending on the type of company. As a private commercial television tends to focus on programming and sales, on public television, the production tends to be the area where the management control expends more effort. The functions of management control in each area can be summarized as follows (Geisler, 2000):

3.4.2 - Production According to Geisler (2000), the main activities related to management control in production are divided as follows:

Despite the development and selection of new programs and ideas to be a responsibility of the director of programs (or information), participation of the controller is particularly desirable in the evaluation of costs and income potential of the various proposals. In his study on the control of management in German TV market, Geisler (2000) found that the higher the level of domestic production, the higher the participation level of the controller. The involvement of controllers in production was found to be higher in public television. As for the instruments used by more management control, are the definition of standard costs and analyze the variation in spending. Although not widely used, more sophisticated tools such as target costing would apply perfectly to the production of programs, since they have strong similarities with the R & D Programme. The limit-factor costing and activity-based costing (ABC) are not widely used. Among the main problems in the management control of production, the study of Geisler (2000) identified the difficulty in calculating the standard costs, the little control on the development of new programs and the difficulty in assessing the external production. 3.4.3 - Programming Geisler (2000) concludes that the area of programming the controller's work focuses on budgeting, planning support and coordination of different plans. Again, the type of control function of management reflects the different focus and mission of television:

The main instruments of management control in the area of programming are used for the management of the stock of programs aimed at measuring the efficiency of its use in programming. In a commercial television company, multi-dimensional allocation of expenses is an essential component of accounting, once you select and schedule programs to produce audience is the core business process. The most common objects of cost may depend on time (slot / slot, day-part, day, etc.) or organization (program, department, gender-channel, among others). This analysis will be essential to measure performance and profitability of programming decisions. The amortization method adopted for the programs will influence the evaluation of profitability, since the amount of amortization will directly influence the discharge of spent. In the study by Geisler (2000), the major difficulties for the management control of the programming area was the difficulty in pricing the individual programs purchased through a package, query the controller very late and this negative image. 3.4.4 - Sales In much of television stations, advertising sales are delegated to agencies. Thus, the management control in this area turns out to focus more on planning and calculation of income. The most widely used instruments in this area will be the reporting and analysis of variation of income. The main problems identified in the study of Geisler (2000) is the perception of poor capacity utilization and the confusing prescription discount policy. 3.4.5 - The Office of Management Control Most German television stations studied by Geisler (2000) has a decentralized management control where the controller reports to the manager twice the area that controls (production, program, sales, etc.) and charge control (or CFO). In the study by Geisler (2000), among the tasks and tools which have been given higher priority and importance in the past, the controllers are:

|

|

||||||||||||

nunofonseca.com - All rights reserved.