| ||||||||||||||

| ||||||||||||||

|

|

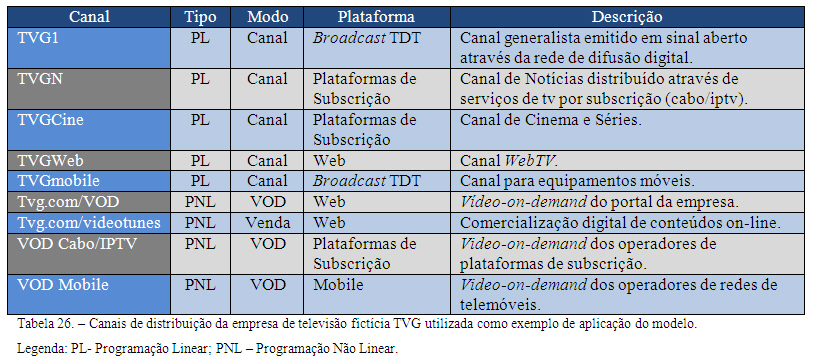

5.5 - Segmented Financial Performance Analysis 5.5.1 - Introduction Segment Distribution Channels Aiming to demonstrate the implementation of the proposed model will be considered a fictitious company called TV TVG - Global TV, comprising the following distribution channels:

Many of the expenses or income may not be directly allocable to a distribution channel, so the following will be created valuables "common" to avoid the arbitrary distribution of values:

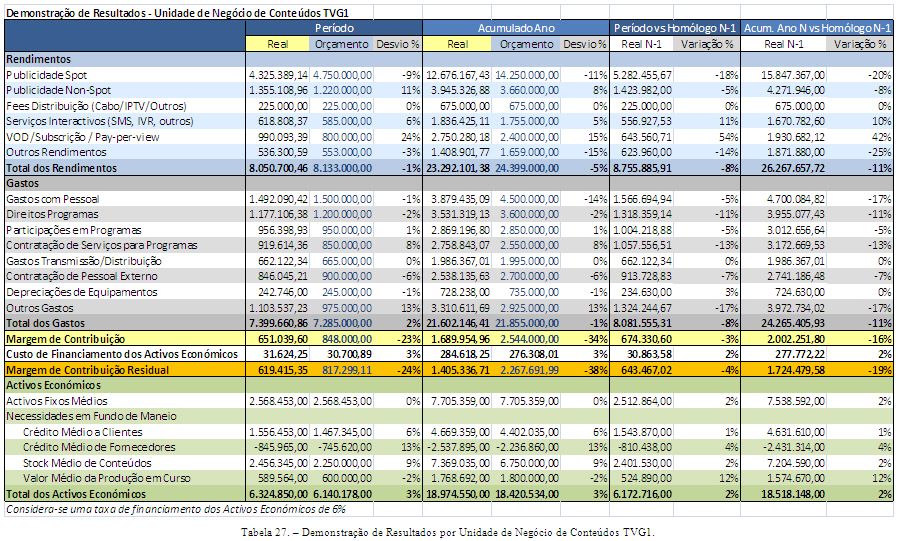

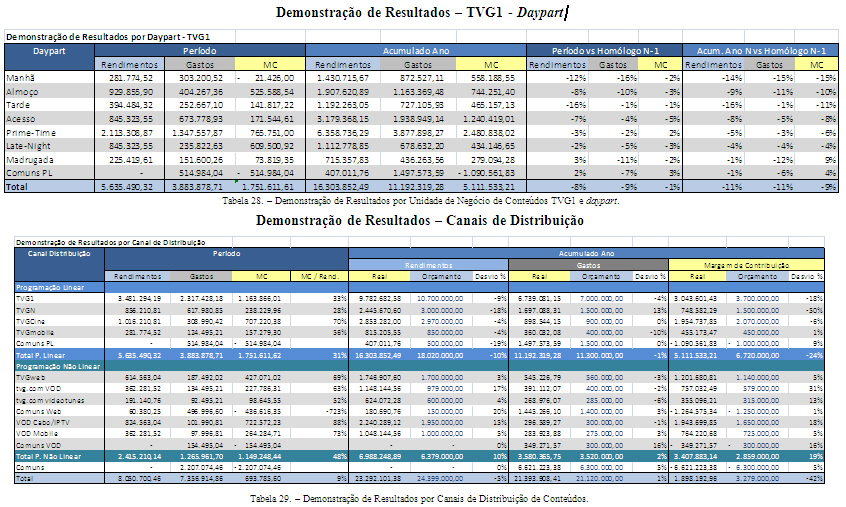

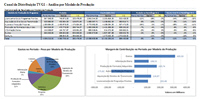

Timeslot Segment Once the type of distribution does not fit this linear concept, is created an object costing "Nonlinear Programming" that will aggregate all expenses and income used to this type of distribution. Will also created a valuable "Common Linear Programming" with the aim of bringing all the expenses and income used to this kind of distribution, but not directly assigned to any timeslot. 5.5.2 - Income Statement by Segment For the evaluation of performance by segment, compared to the theoretical framework introduced earlier, understood as the most appropriate indicators and EVA ® Residual Contribution Margin. Apart from the UNC, the segments shown do not include assets and liabilities. Thus, UNC will be used for the contribution margin Residual considering therefore a funding rate of economic assets to discharge the cost of capital. We chose this measure instead of EVA ®, since it has all the advantages of avoiding this indicator, however, need clearance from the tax by segment. In the evaluation of the remaining segments will be used as an indicator of performance, the contribution margin. This indicator is identical to MCR not considering, however, the cost of financing the economic asset. It applies, therefore, the segments that do not include assets and liabilities, investigating itself, so the segment's operating result. The statements of income resulting from the application of any model. Are presented in the following pages show three examples of results, however, in the annex to this paper presents a model of reporting for the sector will eventually be a result of all the proposed model and an example of the many perspectives and dimensions of analysis . Income Statement - TVG1 - Dayparting

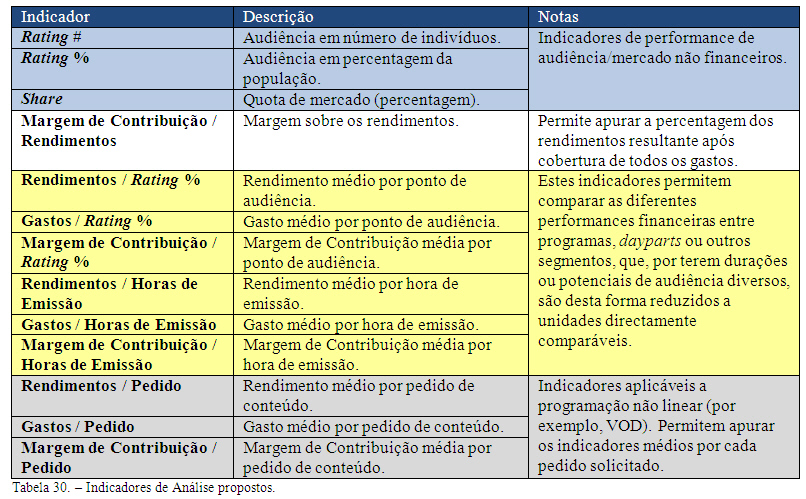

5.5.3 - Other KPI's Analysis In addition to indicators directly computed by the application of theoretical concepts adopted in the model, for example, the contribution margin Residual are proposed at this point, other indicators capable of transmitting information considered relevant in analyzing the performance of this business.

|

|

||||||||||||

nunofonseca.com - All rights reserved.